Crypto Insurance Cover 101

Crypto Insurance Cover 101

Fairside Network, Decentralized Cost Sharing Network

TL;DR

Crypto insurance products are promising, but insurance companies are hesitating for several reasons.

Nexus mutual is the first DeFi insurance protocol which you stake on protocols which you want to cover.

Fairside Network is decentralized cost sharing network which tackles the problem of existing DeFi insurance protocols.

Crypto Jungle

Crypto industry is a jungle. As it is said that a day in crypto industry is a month in another industry, new technologies and projects are emerging and disappearing everyday. As a side effect, things that barely appears in other industry, such as hacking, fraud, scams are appearing every week in crypto.

According to the biggest DeFi bug bounty platform Immnuefi, total loss from hacking, protocol’s technical vulnerability or error in 2021 is about $10B. What Crypto.com, Cream finance, Klayswap, Qubit, and Wormhole have in common is that they had some loss event in 2022. It’s quite impressive in that about 50 days have passed since 2022 at the time of writing.

Watching above incidents with my own eyes, I wonder why I’ve never heard of crypto investors who bought crypto cover products. So, in this article I’ve explored the current crypto insurance landscape and protocols trying to solve this problem.

Insurance 101

History of Insurance

Insurance began thousands of years ago B.C. One interesting point is that insurance have evolved according to the industry development and demand for the insurance.

For example, the first form of insurance, marine insurance emerged in the age when the maritime trade was popular. Fire insurance appeared in industrial revolution when many houses were damaged by fire accidents. Car insurance appeared in 19th century when car supply rate was increasing.

What can be seen from this is that insurance would have no choice but to emerge in crypto industry.

Stance of Incumbent Insurance Companies

Why didn’t existing insurance companies entered crypto industry, when there’s no other industry that grows as as fast as crypto and investors' demand for insurance is so high due to unpleasant loss events? This is the reason why.

First reason is absence of data. Insurance is product based on data and statistics. For insurance companies, crypto is newborn industry without sufficient data for them. However, because of the characteristic of blockchain, every data is opened and transparent, so I think this issue would be addressed shortly.

Second one is absence of domain knowledge. This would be the main reason because it’s hard to find someone with enough crypto knowledge outside of crypto industry. Because insurance companies lack sufficient domain knowledge about crypto and blockchain, they may be discreet to enter this industry.

Last but not least, crypto has so much diverse loss cases. In hacking, it ranges from blockchain protocol itself to front-end and domain. Outside of this, there are smart contract vulnerability, error, rugpull, oracle issue, exchange hacking, flash loans and much more. Moreover, it’s very likely that new loss event would constantly appear in future.

Nevertheless

Nevertheless, there are few companies that offers crypto insurance solutions. However, most of them target exchanges or crypto wallet services. In case of Lloyds, they launched new crypto wallet insurance for coincover and also offers insurance to Crypto.com.

But, large number of unpleasant loss events are not covered by above solution, and what matters is the insurance solution for retail investors, so they can invest without the fear of hacking.

Fortunately, I was able to find projects such as Nexus Mutual and Fairside Network, which are trying to solve these needs.

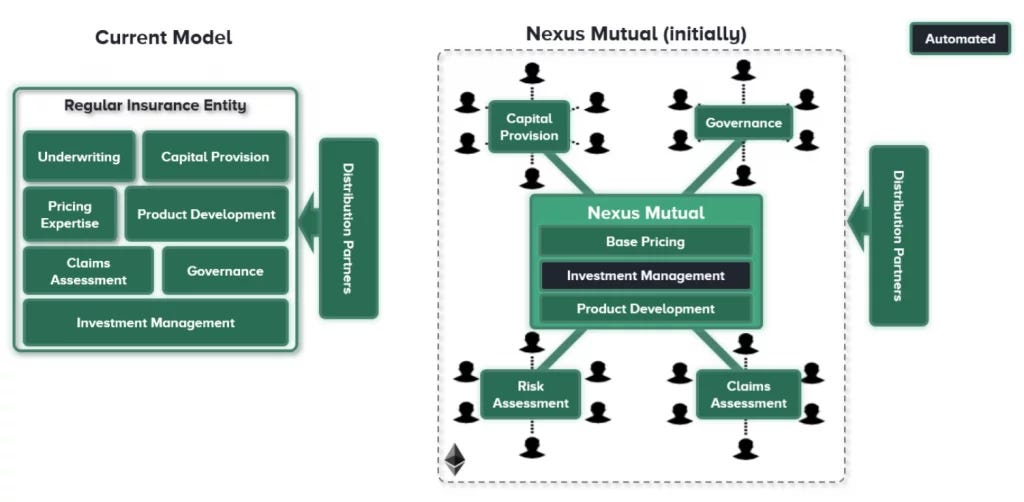

Nexus Mutual

Nexus Mutual is the first decentralized insurance protocol.

Goal

Goal of Nexus Mutual is to eliminate the unnecessary cost and data asymmetry between the trust-needed relationship between insurance company and customer using blockchain.

Existing insurance companies focus more on how to reinvest their profits than customers. But in Nexus Mutual, because insurer and customers are both rewarded by NXM, membership token of Nexus Mutual, they have aligned incentives.

Roles

There are 3 main roles in Nexus Mutual. It’s cover buyer, risk assessor, and claim assessor.

Cover buyer

Cover buyer are literally person who buys cover of specific project to get insured for certain type of loss events. If the corresponding loss events happens through claim assessment, funds are covered.

Risk assessor

Risk assessors are mostly code audit expertise or capitalists with the help of expertise. Risk assessors are those who bet on ‘project is secure’ side. Risk assessors stakes some NXM in cover product and guarantees the safety of the corresponding project.

Risk assessors are rewarded on 50% of cover product premium when people buy the corresponding cover product. However, if the loss event occur and claim assessment happens, staked NXM will be burned to cover the cost.

Claim assessor

Claim assessor votes on whether Nexus Mutual will cover the certain loss event of cover buyers. They vote based on the information submitted by the cover buyers. To become claim assessor, you must stake certain number of NXM. Claim assessor are rewarded when they vote on consensus outcome and staked NXM are burned when malicious voting is done.

How it works

How to buy cover

To buy cover, you should first become the member of Nexus Mutual. It needs some ETH and KYC. After that, you choose the project that you want to be covered and set cover duration and cover cost.

Claiming loss event

If the corresponding loss event occur in the project that I’m covered, cover buyers can register claim assessment. Then claim assessors vote on this claim assessment and if the outcome is to cover, cost is paid from the staked NXM of the risk assessors.

Fairside Network

Honestly, I don’t see Nexus Mutual as a success. Although Nexus Mutual had many advantages as the forerunner of DeFi insurance protocol, it’s hard to find real use cases. Therefore, I have more expectations for the Fairside Network, which uses completely different approach from Nexus Mutual.

Problem of Existing DeFi Insurance Protocols

With the advent of Nexus Mutual, other DeFi insurance protocols followed the mechanism of Nexus Mutual. In most cases, they made independent cover product for each projects and those who bet on the security project and those who bet against it are paired each other. This mechanism is called Project staking.

The fundamental problem of Project staking is the absence of diversification. Basically, it’s very risky for contributors to stake in specific project and to diversify the risk, staking per projects are not appropriate in first place. Additionally, it’s very inconvenient for users because if I use several DeFi protocols, I have to buy each cover products and if the cover product doesn’t exists, I can’t be covered at first place.

Goal

Fairside’s goal is to make a cover product that covers multiple loss events. If you join Fairside membership, regardless of type of project, event and chain, you can be covered if you pass the claim assessment.

Because certain amount of capital is guaranteed through Fairside, existing crypto investors can make profit by investing larger amount of capital in DeFi and new investors can enter the crypto investment.

How it works

Cost Sharing Benefit Model

Fairside maintains the proven insurance industry’s business model and added decentralization by DAO. In fact, strictly speaking, Fairside doesn’t offer insurance product, but offers membership for cost sharing benefit. In other words, Fairside members pay membership fee and promises to share the cost for future unpleasant loss events. These loss events are not limited and decided whether to include it in cost sharing benefit depending on community’s vote. Unlike existing cover products, this approach can handle unexpected loss events more flexible.

Network Staking

Different from Project staking, if contributors bond ETH into Fairside capital pool, they stake in entire network, not specific projects. If we stake on entire network, the correlation between projects we cover becomes extremely low. Also, capital efficiency boosts about 10x from other DeFi insurance protocol and no matter what loss event occurs, participants will not be liquidated.

$FSD

Capital Bonding

By bonding ETH into Fairside capital pool, we can mint FSD. FSD represents my proportion of total Fairside capital pool. Because every FSD is earned through captial bonding, owning FSD means that you are staking in FSD.

Capital Withdraw

If we sell FSD or withdraw capital from the pool, we burn FSD and pay 3.5% tribute fee. If someone withdraw his fund from the pool, total value of capital pool decreases and it leads to the decrease of FSD value. To compensate this, we fin 3.5% tribute fee.

Minting price of FSD

Minting price of FSD is correlated to the adoption of Fairside. As total value of capital pool increases, minting price of FSD increases.This model is made to compensate the early contributors and to guarantee the Fairside’s cover capability to future loss events.

Non-permanent Staking Loss

What’s unqiue about FSD is that unlike the Project staking, if someone claims cover, my capital is not permanently loss(burned).

For example, let’s say someone claimed cover through Fairside. Then, as some fund has been withdrawn from captial pool, price of FSD will drop. However, the number of FSD I own doesn’t changes. Because of this, in Fairside, contributors don’t have to worry about liquidation. Also, as price drop motivates more deposits into capital pool, soon FSD price will pump back, so non-permanent staking loss will likely to be temporary.

Cover Claim Assessment Process

Information Sharing from Lead Assessor(LA)

When loss event occurs, as Fairside decides whether it will cover the event or not by community vote, it needs some entity that can present some objective technological information about the loss event to the community. This entity is called Lead Assessor(LA) and blockchain & cybersecurity firm Halborn Security is taking this role. LA doesn’t affects the vote, it just gives the enough information to community.

Vote from the Members

After looking through the information, Fairside members vote on whether this loss event fits to the cover criteria of Fairside. This criteria may be like ‘does project have minimum 2 audits’, ‘does project members are doxxed’, or ‘does project has operated for at least 18 months’. As members doesn’t know who and how many members have affected from the loss event and have no worries about liquidation, they can vote fairly.

Proof-of-Loss Submission

Fairside members which have suffered from the loss event that passed the community vote, members could submit Proof-of-Loss to LA. If LA approves the submission, members can get covered and if it’s denied, members can appeal. Regardless of the outcome, members who submitted Proof-of-Loss pay proportion of membership fee to members who participated in the vote.